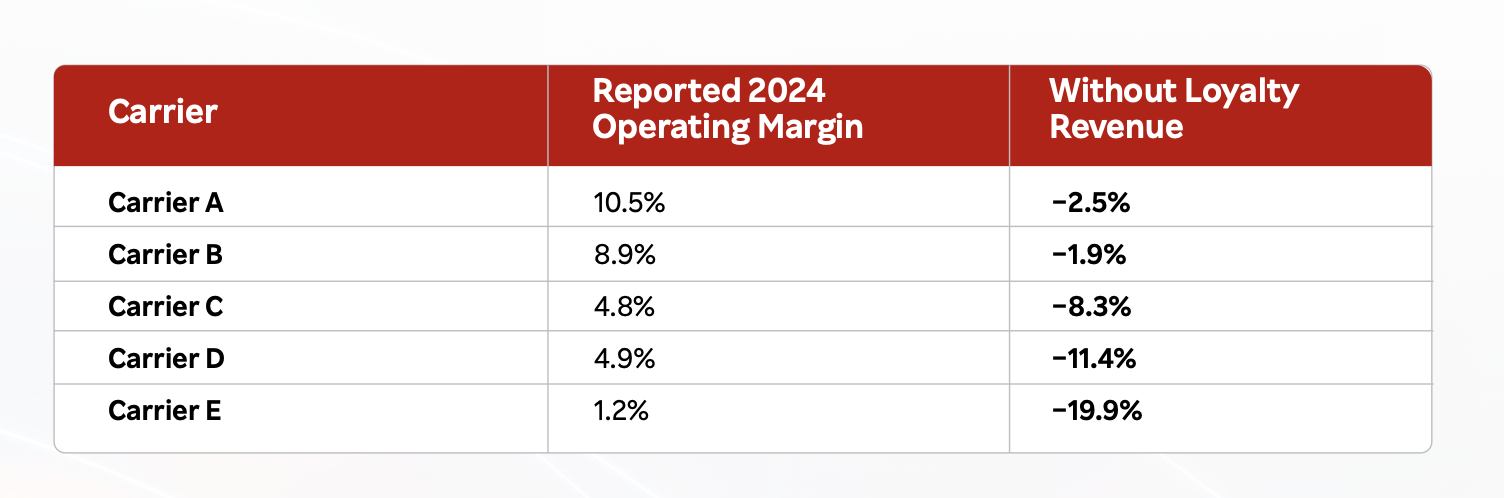

Did you know that the entirety of the profit of a major airline is made up from money it earns from its loyalty schemes? That is to say, without their air-miles schemes, the airlines would turn a loss. And whether you did or didn’t know what, would you be able to say why that is relevant to the telecoms industry?

Taken from the Rakuten Symphony “Industry Growth Report”.

This piece of dinner-party bait is laid out within a new report published today by Rakuten Symphony, titled the 2026 Industry Growth Report.

The report was written by Geoff Hollingworth, Rakuten Symphony CMO and prolific LinkedIn poster and debater.

For Hollingworth, the industry has got itself into a strategic muddle, acting as one thing but operating as another. As he lays out in his report, individual telcos urgently need to decide what they are, and then redesign their operating model, technology, partnerships, and customer proposition around that choice.

Discussing the report with TMN, Hollingworth argues that operators have become caught between competing identities. Should they sell and compete on price and quality of connectivity – essentially act as utilities? Should they design themselves around the platform model? Should they become ecosystem partners and enablers, like Rakuten Mobile is able to do in Japan?

The report offers three paths to choose from.

Some companies may choose to become highly efficient connectivity utilities. Others may seek to build platform businesses around the network: the Network API model we are seeing from many. A third route is to act as partners within broader ecosystems.

None of these are bad choices, and there are examples of all three in the industry. What matters, Hollingworth argued, is that operators stop trying to be all things at once, or acting in one direction and talking in another.

“What I’m saying is the companies that are already doing well have decided an identity that leads into a customer promise,” he said. “They start to design their business around that identity and around that promise.”

For an industry still searching for growth beyond connectivity, that may be the most important strategic choice of all.

So let’s take the first path – accept the connectivity provider as utility path. There is “absolutely nothing wrong” with telecom operators choosing to be connectivity utilities, provided they fully embrace the model, Hollingworth said.

“If you choose to do that, you need to be a brilliant connectivity provider. You should have best-in-class operations based on delivering those metrics.”

He pointed to Lumen’s work with hyperscale customers as an example of an operator reshaping its business around a clearly defined customer segment. By focusing on connectivity for hyperscalers, the company was forced to redesign operational processes, inventory systems and service interfaces to meet stringent service-level requirements. And it was also able to ignore a lot of the rest of the technical bells and whistles that telcos design for themselves.

What telcos shouldn’t do is price and behave like utilities, yet continue to invest and organise themselves as if they were high-growth technology companies.

Build the ecosystem

Even so, while many telecom operators continue to market network quality and coverage improvements, and is facing a new technology upgrade cycle with 6G, Hollingworth suggested that connectivity alone is becoming an increasingly weak basis for customer differentiation.

“Our recommendation is that telcos really need to start looking at how they can promise customers something different from base connectivity and ‘best 5G ever’, which they pay a huge amount of money promoting,” he said.

Instead, he advocated building broader customer propositions through partnerships with companies in adjacent industries.

To illustrate the concept, he pointed to the airline industry, where loyalty ecosystems have evolved into powerful business platforms. Airlines generate significant value by connecting customers with hotels, car rental companies and credit card providers, all of whom are willing to pre-pay for access to airline customer relationships. If you want to understand much more about how loyalty schemes work, and the economics involved, then do read the report.

“The airline industry is interesting because the actual mechanisms are so transparent in terms of how this works,” he said. “It’s so obvious how lucrative it is to have relationships and cross-selling.”

The lesson for telecom operators is not necessarily to build airline-style loyalty programs, but to create economic partnerships that lower customer acquisition costs for participating businesses while increasing customer retention.

Learning from Rakuten

The guiding light of a telco that has had some success in this area is Rakuten Symphony’s stable-mate Rakuten Mobile. Rakuten’s customers are called “members” not subscribers, and they earn points when they interact with multiple parts of the Rakuten business.

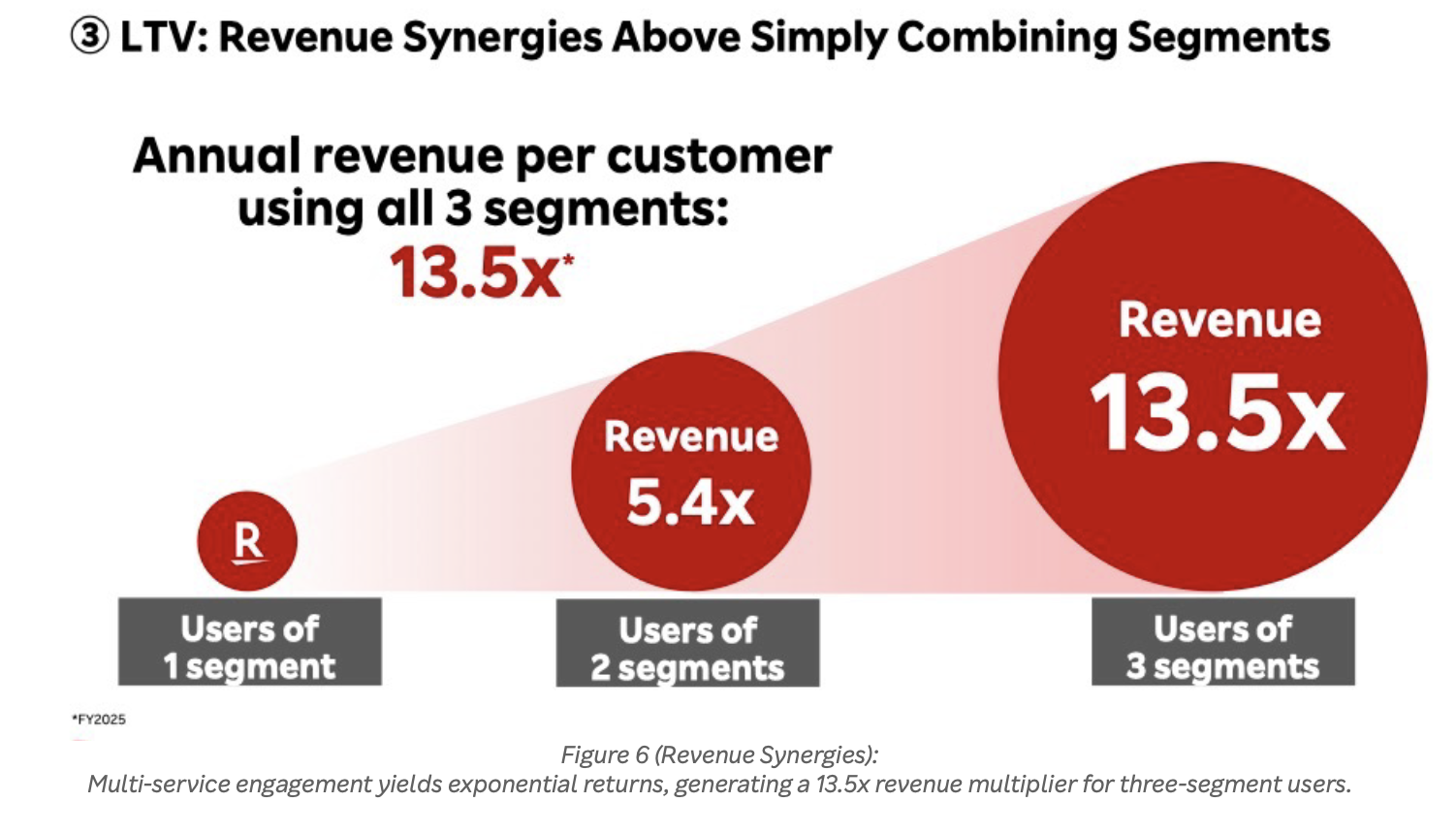

And the report and Hollingworth claim that customers who engage with multiple Rakuten services generate significantly greater value.

“If there was a customer that uses the mobile service, finance and internet, they generate 13.5 times more value,” he said.

As well as build revenue the model also builds stickiness. Customers that use four services churn are one hundred times less likely to churn, Hollingworth said.

Those outcomes, he argued, stem from creating value propositions that extend beyond connectivity and become embedded in customers’ everyday lives.

Making it work

But is Rakuten really a good example for the industry to follow? It began as an e-commerce company and gradually expanded into banking, payments and credit and travel. The mobile operator was added to an existing ecosystem.

And can standalone telcos find their business partners and make the airmiles model work? Would customers engage with a loyalty scheme run by their telco? Would you?

“Look, my air conditioning company runs a loyalty scheme,” he says, “and I’m happy to be a member of it because I know if my aircon dies on the hottest day of the year, the company will come out and see me.”

Where a telco can come up with partnerships that reduce acquisition costs for the partner, those savings can then be used to fund a better experience for the customer, Hollingworth said.

Then there’s execution – following the partnership model seems to build a whole business function that doesn’t exist in the majority of telcos, at least not beyond the people who are responsible for organising discount tie-ups with content and entertainment partners such as Netflix and Spotify. Hollingworth would no doubt argue that making a choice to follow that road would actually free up resources and effort currently spent chasing the current business model.

And he readily admits the obvious self-interest in Rakuten Symphony promoting the report. The company sells the technology that telcos can use to mine customer data, come up with offers and then execute on programmes and partnerships. And of course it wants to encourage different modes of thinking in order to encourage a healthier customer base.

Should technology lead

Aside from anything else, the Report works out what is clearly a personal bugbear for Hollingworth – telco’s technology-first mindset.

He said telecom conferences are dominated by CTOs discussing future technologies while avoiding harder questions about customer value, business models and competitive positioning. The report certainly doesn’t do avoid any of those issues.

As we move into DTW Ignite next week in Copenhagen, it seems there will be at least one industry CMO counting the number of business people driving discussion at the industry’s biggest dedicated IT and network operating systems event.

Comments

0